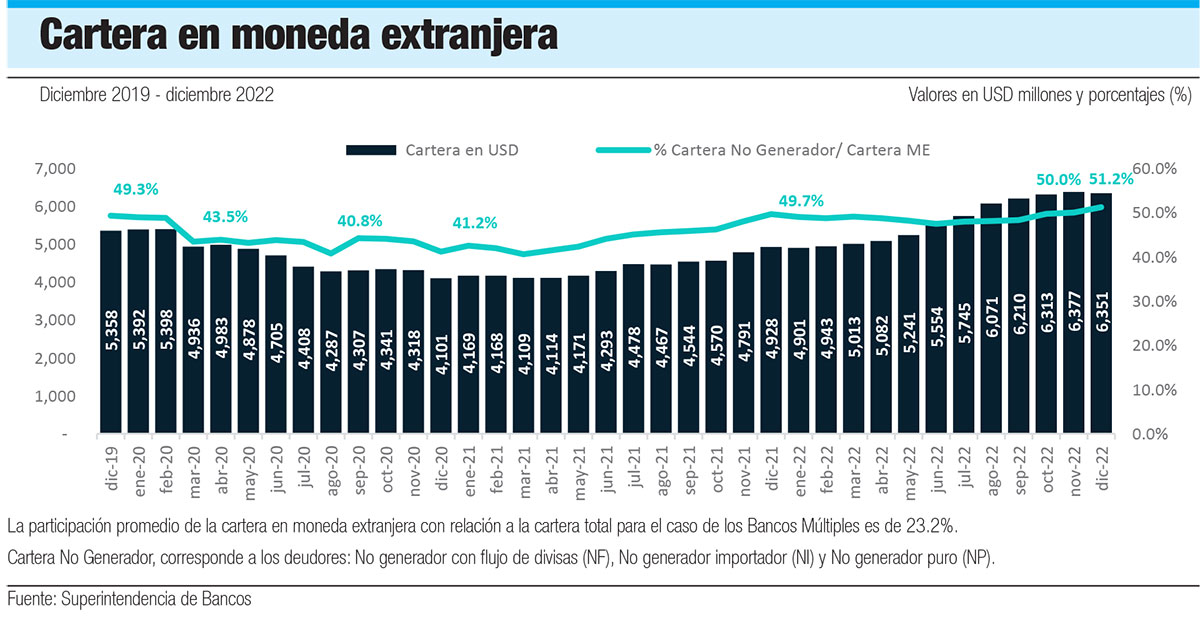

The foreign currency loan portfolio of Dominican banks closed 2022 at US$6,351 million, of which US$3,550.2 million, 55.9%, is concentrated in four sectors: tourism (22.2%), industry (12.3%) and 21.3% for commerce and financial activities and insurance.

Based on these data, available in the “Report on the behavior of the foreign currency portfolio”, published by the Superintendency of Banks (SB), tourism is the sector with a total debt of US$1,409.9 million, while the industry closed 2022 at US$781.2 million. The rest accumulates a debt of US$1,352.8 million.

The Superintendency of Banks highlights that the Dominican financial system has shown wise management of the risks derived from exchange rate fluctuations in the loan portfolio, which is evidenced in the performance in foreign currency.

“This has presented an important participation in the period before and after the pandemic, which is a good indicator that reflects the expectations of the economic agents on the performance and quality of said portfolio”, states the institution in the report published in April.

The data establishes that the foreign currency loan portfolio grew by 28.7% compared to December 2019, placing it at the end of 2022 with a weight of 22% of the total portfolio.

It indicates that at the end of December 2019, the period prior to the pandemic, the share of the foreign currency portfolio stood at 23.1%. However, by the end of 2020, it presented a reduction of 4.1 percentage points as a result of the effects of the covid-19 pandemic. In this order, it refers that the ratio of the portfolio in foreign currency over the resources captured in foreign currency corresponding to 43.3% as of December 2022.

“By December 2019, the ratio of the foreign currency portfolio over resources raised stood at 50.8%, presenting a variation of 7.5 percentage points. The levels of delinquency for the financial system and foreign currency portfolio show a downward trend”, as reported by the SB, highlighting that it remains below the system’s records, as it is at 0.4%.

Provisions

One of the variables that stands out as positive is the coverage ratio of provisions over the non-performing and past-due portfolio, as it shows significant and constant increases since April 2020 to date. As of December 2022, the provisions made in foreign currency cover more than eight times past-due loans.

However, the foreign-currency portfolio granted to pure non-generators as of December 2022 represented 24.6%. For this segment, it highlights, there has been a significant increase in guarantee coverage, which, by the end of 2022, stood at 64.8%, which, in the opinion of the financial authorities, evidence that for every 100 pesos lent, 64.8 are covered by guarantees, showing the tendency of the entities to cover their risks.

Exposure

For the Superintendency of Banks, a significant factor that may materialize the credit risk of default in an economy such as the Dominican Republic is the fluctuation of the exchange rate, for which reason the follow-up and correct control of the exposures in foreign currencies by the financial intermediation entities (EIF), especially to debtors that do not generate foreign currency, is of great importance.

It points out that a correct risk selection criterion and sufficient hedging of exposures by the supervised entities, together with specific, robust, and measurable prudential guidelines by the agencies that make up the Monetary and Financial Administration, are fundamental for risk mitigation.

For the periods of uncertainty derived from the covid-19 virus containment measures and in the face of the rise in the exchange rate, the entities reduced the portfolio share to 18.2% of the total.

Total in pesos

The Superintendency of Banks (SB) establishes, in its report as of December 2022, that the credit portfolio of the financial system amounted to RD$1.61 trillion, for a year-on-year growth of 14.8% in nominal terms, surpassing the levels shown in the last seven years with an average of 10.1%.

It highlights that the loan portfolio continues to be the most important component of the total assets of the financial system, representing 53.9%. However, it indicates that it has experienced a reduction in its participation of four percentage points (year-over-year), placing it below the average of the last five years of 57.6%, given the context of the pandemic and the policy measures to counteract its effects.

Multiple banks and savings and loan associations have a 97.1% share. The remainder is in savings and loan banks (2.5%), credit corporations, and public financial intermediation entities, both with 0.2%.

Source: