- Updated global figures point out that Latin America and the Caribbean face a scenario of moderate and uneven growth in 2025

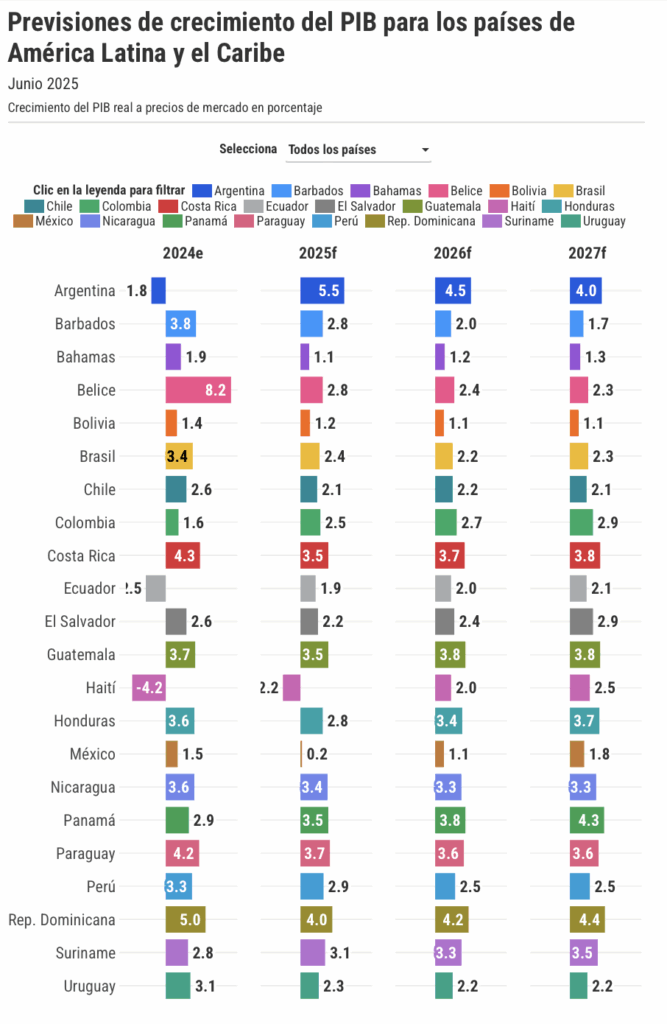

he World Bank lowered its January growth projection for the Dominican economy in 2025 by 0.7 percentage points, by reducing the real gross domestic product (GDP) from 4.7 to 4.0%.

However, the country remains among the economies in Latin America and the Caribbean with the highest projected growth, “as it benefits from structural reforms aimed at attracting foreign investment,” according to the World Bank, while forecasting an average growth of 4.3% for 2026-2027.

In its World Economic Prospects report, released on June 11, the World Bank points out that Latin America and the Caribbean are facing moderate uneven growth in 2025, in a global context marked by the resurgence of protectionism, political uncertainty and trade tensions with the United States.

According to the World Bank, regional growth is expected to remain stable at 2.3% in 2025 and increase slightly to 2.4% in 2026, as growth weakens in most economies, except Argentina, Colombia, Ecuador and the Caribbean.

Mexico, the economy most integrated with the US, will be particularly affected by the new trade barriers imposed by Washington, with 25% tariffs on products that do not conform to the USMCA.

This situation has increased uncertainty around the bilateral relationship, at a time when around 80% of Mexican exports are destined for the U.S. market.

Mexico and the Caribbean, the most vulnerable to U.S. protectionism

Mexico’s strong exposure to North American supply chains makes the country the most vulnerable in the region.

Mexico’s real GDP growth forecast for 2025 was revised significantly downwards, from 1.5 percentage points to 0.2% in 2025, and the country will grow by 1.1% in 2026.

Manufacturing exports will decline, and although interest rates are falling, they are expected to remain high. This monetary policy, together with a declining fiscal deficit, will limit the expansion of domestic demand.

Central America and the Caribbean are also highly exposed. The Central American economy is expected to grow by 3.5% in 2025 and 3.6% in 2026, supported by services exports and improved consumption.

Costa Rica leads with a forecast of 3.5% real GDP growth in 2025 and 3.7% in 2026, thanks to energetic domestic consumption.

Panama, for its part, would reach 3.5% in 2025 and an average of 4% in the following two years, thanks to the rebound in trade in services linked to the Canal.

In the Caribbean, the most prominent case is Guyana, whose real GDP will expand by 10% in 2025 and an average of 23.65% in 2026-27, driven by investment in oil.

The Dominican Republic is also solid, with 4% in 2025 and 4.3% in the following biennium, while Jamaica will have moderate growth of 1.7% on average between 2025-2027.

- In contrast, Haiti’s economic outlook remains fragile and highly uncertain amid persistent political instability and security challenges, with the economy expected to contract by 2.2% in 2025.

Argentina, Colombia and Peru: disparate dynamics

According to the World Bank, Argentina will resume growth this year with a rate of 5.5%, after two years of recession. The recovery will be supported by agriculture, energy and mining, and will be accompanied by macroeconomic stabilization policies, elimination of exchange controls, and pro-market reforms.

An average growth of 4.3% is expected for 2026-2027. The Argentine government plans to maintain sustained fiscal surpluses in line with its program with the IMF.

Colombia is also on track for a moderate recovery, with growth of 2.5% in 2025 and an average of 2.8% in 2026-27. This improvement is based on a rebound in private consumption and a slight recovery in investment, supported by looser monetary conditions and inflation that continues to decline.

However, political and economic uncertainty could hamper a more robust recovery.

Peru can expect a 2.9% expansion in 2025 and an average of 2.5% in the following years. Weak domestic demand, uncertainty about domestic policies, and fiscal consolidation explain this moderation.

Nonetheless, mining investments—especially copper—and infrastructure projects will provide an anchor for growth.

Brazil and Chile face internal and external challenges

Brazil, Latin America’s largest economy, will face a significant slowdown: from 3.4% in 2024 to 2.4% in 2025, and an average of 2.2% in 2026-27.

Lower investment and weaker consumption weigh on growth, although the reduction of interest rates (from 13.75% to 10.5%) should alleviate some of the inflationary pressures. Fiscal sustainability will be key to stabilizing the Brazilian economy, which still faces market doubts.

2.1% growth is expected in Chile in 2025 and an average of 2.2% in 2026-2027.

The report highlights an expected recovery in domestic demand and mining investments in Chile, especially for copper and aluminum. However, institutional uncertainty persists, which could hamper investment, particularly in mining and technology.

Structural factors holding back regional growth

The World Bank report warns that, despite an incipient recovery, Latin America and the Caribbean will continue to be the region with the lowest growth among emerging markets and developing economies (EMDEs). Factors such as low productivity, a less-educated workforce, and an aging population weigh on long-term prospects.

The region also faces macroeconomic risks. More than half of LAC economies have seen downgrades in their growth projections.

Inflation, although falling, remains above central banks’ targets, and interest rates will remain high to consolidate fiscal stability. This environment will limit the space for expansionary policies in the short term.

In addition, the deterioration of the fiscal accounts after the pandemic and higher borrowing costs could force more severe adjustments than expected. The report warns that these cuts could have contractionary effects on regional growth.

Dependence on China and the US, key to the economic future

Economic relations with China also strongly influence the forecasts. A slowdown in Chinese demand — especially for metals — would affect the prices of commodities such as copper, with direct impacts on Chile and Peru.

For its part, any contraction in U.S. growth would have negative multiplier effects in Mexico, Central America, and the Caribbean, particularly due to the fall in remittances, tourism, and exports.

Latin America and the Caribbean remain highly vulnerable to global ups and downs. Despite some positive signs, such as Argentina’s recovery or resilience in Guyana and the Dominican Republic, the report concludes that internal structural challenges, coupled with external trade tensions, will continue to set the pace for a recovery that is still uncertain.

Source: